Futures And Forwards

Interest Rate and Treasury Futures Primer

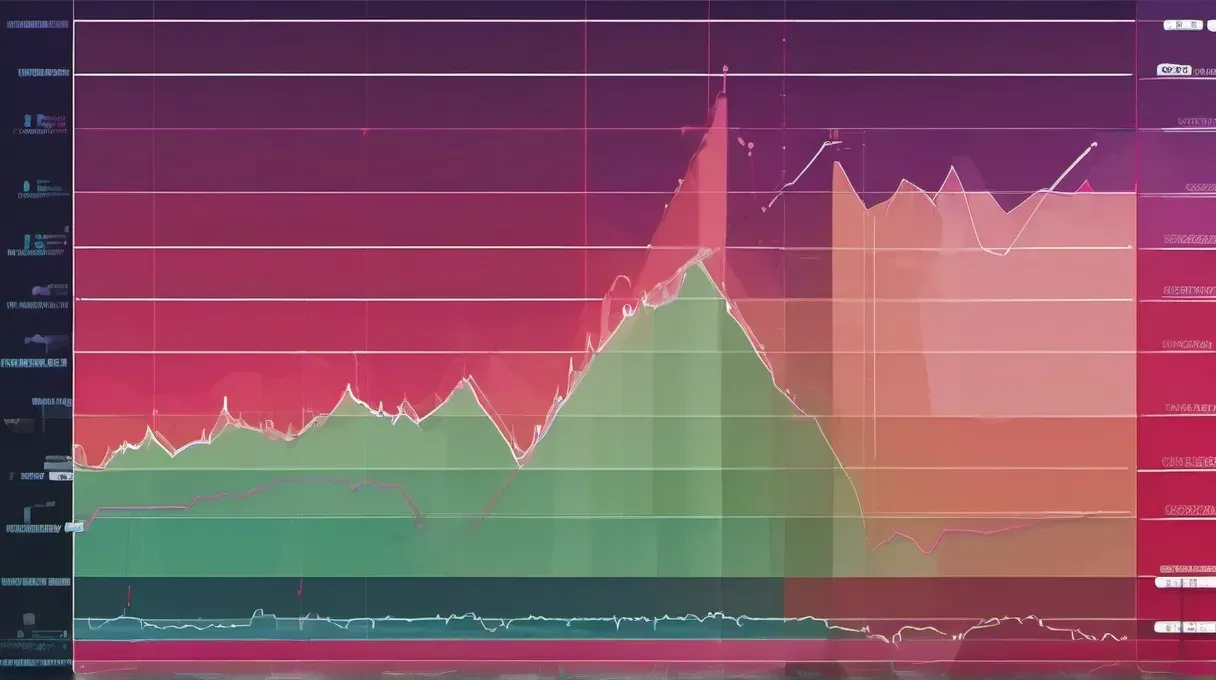

Treasury futures are the most actively traded derivatives contracts in the world—14.2 million interest rate futures contracts per day across CME products in 202…

intermediate 2026-01-31